Today’s US energy market is transitioning from its traditional high-carbon roots to a low-carbon future. This new energy market will have a different economic structure and will require different infrastructure. These changes will mean that some existing assets and existing asset infrastructure won’t be economically viable anymore.

In the electric power space, we’re already seeing the effects of this transition:

- Renewable energy and distributed energy resources (DERs) are replacing older electric and gas generation systems, like coal-fired power plants, to provide a cleaner and cheaper source of power

- Utility energy efficiency and DER programs are helping customers use less energy and switch from gas to electric technologies

- Utilities are replacing millions of analog meters with digital advanced metering infrastructure technology

- More battery storage is coming online and will reduce or eliminate the need for spinning reserves

This transition can happen quickly and may happen before utilities are fully prepared. This creates the potential for some of these assets—including generation, transmission, and distribution systems—to become economically “stranded.”

Stranded assets are those that are no longer financially viable because they aren’t being used enough to continue to pay for themselves. In the next three to five years, we could see billions of dollars of assets become stranded as a result of shifts in how we use and distribute energy on the grid.

Obsolescence isn’t reserved for electric assets. There’s real risk for natural gas utilities in seeing some of their pipeline infrastructure become stranded. The assessment for obsolescence is complicated, but there are a few things driving change to natural gas economics. These include:

- Changes to greenhouse gas emissions standards by state governments

- Changes to building codes

- Changes to demand patterns based on fuel switching, price, and environmental justice

Natural gas utilities have fared better in regulatory returns than their electric counterparts. And despite the complex formulas determining obsolescence for natural gas assets, issues with aging infrastructure are driving the need for continued investment in these assets for reliability and resiliency.

Can utilities avoid stranded assets? What should utilities do with these assets once they’re stranded?

Utilities in deregulated states may have more options to recover costs. Utilities in regulated states may have a harder time recovering costs if assets within their regulatory structures become economically unviable. This is because regulatory conditions are changing.

Regulators are giving more scrutiny to stranded asset recovery

Regulators are giving greater scrutiny to stranded cost recovery—they’re sensitive to the fact that customers often have to pay the cost of recovering stranded assets. This regulatory sensitivity makes it harder for utilities to recover costs for stranded assets as the industry transitions to a low-carbon market.

Only 8 US states are fully deregulated; 14 states are semicompetitive. Texas is fully competitive, but only those parts of Texas inside the Energy Reliability Council of Texas. The rest of the semicompetitive states are fully regulated by utility commissions. This can be good news for many of the utilities within these regulatory structures.

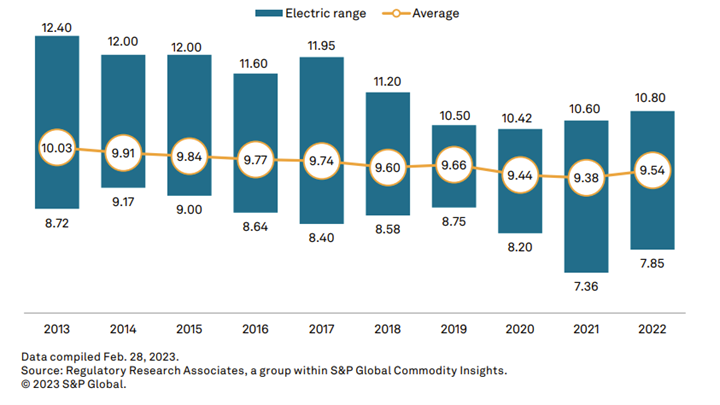

But the authorized regulated rates of return on equity for utility electricity assets have been steadily dropping since 2009 when the rate was about 13%. In 2022, that rate fell to about 8%, according to Regulatory Research Associates, a group within S&P Global Commodity Insights (figure 1). Natural gas utilities have seen a smaller drop in the rate of return on gas assets. This decrease is due to several factors. But the bottom line is that regulators are increasing their scrutiny on what utilities can and can’t include in the cases.

Figure 1: Electric return on equity authorizations, 2013–2022

How deregulation stranded assets at the turn of the century

Our traditional view of stranded assets comes from the late 1990s and early 2000s. During this time, retail competition drove a period of deregulation in the US energy market. The idea was that competitive generation—which included merchant-owned and independent power producer–generating plants—would generate power for less money and would lower the cost of power.

Proponents of deregulation also assumed that these new plants would devalue the older power plants. That was partly correct. The influx of cheap and plentiful natural gas was so rapid that it would also crush the coal-fired power generation sector.

In 2009, about 60% of every megawatt generated in the US was from coal-fired power plants. And these coal plants represented over 300 gigawatts (GW)—or 300,000 megawatts (MW)—of the 1,000 GW of total installed capacity.

At that time, I was at SNL Energy and predicted that 120 to 160 GW or more of coal-fired capacity, and a lesser amount of natural gas capacity, would no longer be useful and would fail economically. That forecast caused quite a ruckus because it was so contrary to the status quo.

Renewable energy is ushering in a new era of stranded assets

A decade and a half later, coal-fired power now makes up about 20% of every megawatt generated. Every state now has a graveyard of retired coal plants. While coal-fired assets continue to generate, most do so under limited capacity factors and rely on cost-recovery mechanisms. This trend will only continue.

The latest Lazard Levelized Cost Of Energy analysis shows that most renewable generation technologies are cost-competitive or even more cost-effective than fossil fuel generation. Another 28 to 30 GW of coal-fired capacity, and some natural gas assets, are at risk through 2025.

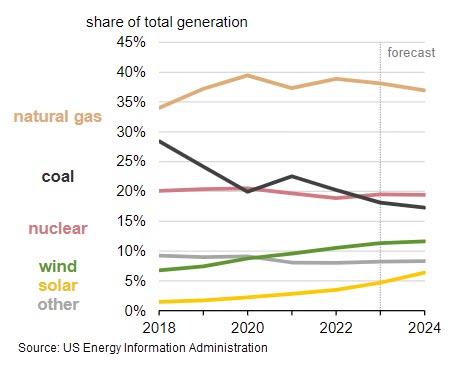

According to the US Energy Information Administration (EIA), almost 9 GW of coal capacity will retire in 2023. Meanwhile, the EIA predicts that solar and wind will account for 16% of US power generation this year (figure 2).

Figure 2: US electricity generation by energy source, 2018–2024

Retail competition created today’s mechanisms for stranded asset recovery

Retail competition created a dark period in US power market history. Utilities convinced regulators to create mechanisms for them to calculate the “future returns” on their assets. This would allow utilities to recover costs through a set of regulatory-imposed economic structures. This system legally allowed utilities to get paid for inefficient generation or for not retiring old plants fast enough.

Policymakers were convinced that utilities should be compensated for this devaluation of their assets. This was our industry’s version of a moral hazard. That may be a controversial viewpoint, but many companies could recover money based on these structures. This lifted many US utilities out of bankruptcy and helped pay millions of dollars in bonuses and fees to CEOs and bankers.

The overall formula to calculate stranded cost obligation is what guides today’s regulatory recovery structures:

stranded cost obligation = (revenue stream estimate – competitive market value estimate) × length of obligation

This formula is based on a time value of money with some extra rules around it, including:

- A rationale that proves that the cost to serve the customer (retail or otherwise) was based on the reasonable expectation that the utility would continue the service; and

- That the stranded costs weren’t more than what the customer would have paid if they had remained a wholesale customer or retail customer.

Recovering assets in regulated states

This period of retail competition created the cost recovery structures that utilities still use today for stranded costs. There are three main mechanisms that regulated utilities can use to deal with stranded or potentially stranded assets. Remember that regulators are sensitive to the fact that customers pay for the cost of these schemes. The mechanisms are:

- Accelerated depreciation of the early-retiring assets

- Creation of regulatory assets that allow them to recover the remaining value of the assets

- Securitization of the asset to sell the revenue streams to interested parties to offset the utility’s cost

Recovering assets in deregulated states

It may seem a bleaker picture for assets in deregulated states, but there are several mechanisms that allow for recovery. Some recovery mechanisms let utilities use state-sponsored subsidies to bail out failing power plants or other assets. Investment banks or investors are responsible for coming up with creative finance structures to avoid bankruptcy.

Securitization is a favored option as a recovery mechanism in deregulated states because it provides a lot of options. Securitization creates a financial structure that lets the owner of the stranded asset reduce the cost or loss by shedding the risk.

There are lots of companies that want to take on this type of risk. Risk comes with a premium—companies usually get paid for the excess risk through a fee or higher rate of interest. And risk-tolerant entities want as much risk as they can get. Companies will adjust the business to make the returns they need. Utilities and asset owners have used securitization to reduce risk for other types of investments, including:

- Early asset retirement

- Green investments

- Extreme weather-related costs

- Environmental compliance

- Reliability expenditures

- COVID-19 revenue or load losses

- Energy conservation

Utilities aren’t the only organizations that turn to securitization to deal with stranded assets and changing economics.

Global energy producer BP had a large effort underway to repower its first-generation, early-2000s-vintage Texas wind plant. The repowering saw bankers and investors lining up to take on the cost (in the hundreds of millions) to upgrade towers—and the power generating kit, blades, and gears—from older 1 MW units to new 4 MW or higher output units. BP chose to reduce risk in its portfolio and sell its Texas wind plant portfolio to Ares Management Corp.